Within a few short years we could find our banking system is bankrupt. No, I’m not trying to predict another subprime mortgage collapse, and this isn’t another anti-Trump message of doom (although his lack of understanding of ‘the cyber’ and affinity with traditional business models will not help the United States of America weather such disruption). Instead, the rise of the ‘Blockchain’ simply renders banks unnecessary.

Why do banks exist?

Banks exist because storing your cash under your mattress isn’t very secure. But what is it about banks that makes them a safer place for your hard-earned wedge?

According to legend, the the Knights Templar invented the first form of modern banking in the 12th century. They would take in money from Christian crusaders, pilgrims and travellers in return for a slip of parchment that detailed their deposit. Further along their journey they could swap their parchment at a ‘Templar House’ for gold, silver and whatever-the-hell-myhrr-is up to the value they had deposited. Sound familiar?

As for security, the Knights Templar were some of the most fearsome warriors around. They didn’t need to chain their pens to the desks, if you nicked one you’d do well if you only lost a hand…

The first Templar banking system relied on low literacy levels. Basically, the hope was that the parchment could easily be overlooked by groups of medieval chavs rifling through your pockets looking for gold coins. Eventually, the parchments were written in code (encrypted) to avoid them being tampered with. Ironically, it is encryption which is the basis for Blockchain, which may end up destroying this old-style of banking.

By the way, the legends are all bollocks because the Chinese Yuan dynasty had banknotes in 1000 AD…

Boom and Bust

Boom and Bust

Banking has evolved little in the centuries since the Templars rose to become global financial giants in the 1100s (remember, the globe was smaller back then as America had yet to be invented). Those slips of parchment became bank notes and bearer bonds; and instead of only exchanging them with the bank, ordinary people began to use them as currency amongst themselves. They became a representation of money stored somewhere and that money was accessible to anyone who held that note.

The Federal Reserve Act of 1913 required the central bank of the US to “have gold backing 40% of its demand notes”. The other 60% could be made up from other assets (property, rare metals, etc.)

But then, as the 20th century progressed, money became less and less tied to real value.

The stock markets created a monetary system largely based on speculation and perception of value allowing events like Black Tuesday on October 29th 1929 to occur, which was the start of the Great Depression.

The rise of Fractional-Reserve Banking practices, which allows banks to lend multiple times the amount they actually have in their vaults (upwards of 9x in the USA) and the expansion of global trade meant local down-turns quickly became significant international crises (such as the subprime mortgage crash in 2008).

Basically, the existing banking system floats on an ocean of 90% made-up cash. And when the excrement hits the fan, i.e. when there is ‘a run on the bank’ and customers start withdrawing more than 10% of the money the bank claims to have, the system implodes. We are walking on a knife edge.

Even more irksome is that banks are able to charge interest and fees on this money that they don’t have; money that is only permitted to exist because you have likely had your wages paid into your account.

Trust in banks is at an all-time low.

Boom and bust cycles are not new, but this time it’s different. This time we are connected as a species at an unprecedented level. We see and hear the pain of those impacted by cock-ups in the financial industry in vivid 32-bit colour on 4K ultra-High-Def flatscreens and, thanks to Blockchain technology and the Internet, we have new ways of keeping our money safe that we’ve never had before.

New ways that do not require banks.

The Blockchain

What if money wasn’t only a representation of value, but also included information about who owned that value? Like writing your name in permanent marker on every bank note in your wallet.

Blockchain uses principles of ‘cryptography’ to do just that, but with a new type of money called a Cryptocurrency. CryptoSharpies at the ready…

Cryptography is the process of hiding information. We’ve probably all played with a Caesar cipher when we were kids, writing encoded messages to friends by shifting the alphabet by a number of characters. This is one of the most basic types of encryption.

As technology improved, the famous Enigma machine from World War 2 used electro-mechanical wheels to generate extremely complex alphabet shifting (even brief study of which will give you enormous appreciation of the sheer genius of Alan Turing). Only by knowing this complex sequence of ‘shifts’ could you decode the messages. This sequence is known as “a key”.

Cryptography is at the heart of secure internet browsing today. Very complex keys are used to secure the channel between your web browser and your online banking app. Those keys are used to encrypt the data flowing in each direction so that only the other end can ‘decrypt’ (or ‘decipher’) it and read it.

If you understand that, you understand the magic behind the ‘padlock’ icon on many websites.

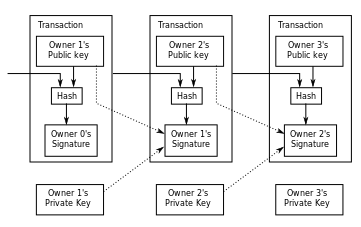

Now let’s say that in order to decrypt a message you have to use the previous message as the ‘key’ for the new message. It requires knowledge of previous keys so you create a chain of messages that are inherently connected, and have a strict, mathematically-provable ancestry: they can be traced back.

Furthermore, if you decrypt something incorrectly you don’t have the key for the next message, and if you try to tamper with a message while it is in-transit, it won’t decrypt properly.

‘Blockchain’ is one of these chains, but instead of messages it contains transactions. The inability to tamper with the transactions, and having a mathematically-provable history to every unit of currency means it becomes impossible to commit fraud and you can easily prove where you got your money from.

Can’t I just create my own chain?

Can’t I just create my own chain?

Yes, you absolutely can, but you’d only be able to trade with yourself and those who trusted you. In our post-truth world, nobody trusts you. (Sorry. Not sorry).

Instead, the race is on to create “The Blockchain”, the Gold Standard of cryptocurrencies which everyone else buys into.

Everybody is on this bandwagon, from ‘private blockchains‘ for securing company contracts, documents and private transactions to credit card companies to blockchain-based secure communications.

Cryptocurrencies operate what is called a ‘distributed ledger’, which means anyone and everyone owns the transactional history of every crypto-coin, but somebody has to create the first transaction for everyone else to link back to.

Bitcoin and its distributed ledger is leading the cryptocurrency race with an astonishing market cap approaching US$12bn and over 100,000 merchants accepting it as payment (including Microsoft, Dell, Virgin Galactic and PayPal). This shows the major players have already overcome their initial fears and are investing heavily.

Would you trust a blockchain owned by your bank? Or have banks had their chance to operate ethically and properly in the global financial system, and blown it?

More to the point, if your money is unhackable and unstealable (supposedly) and lives in a distributed fashion on the internet, do you even need a bank account anymore? (No, you don’t!)

The Big Bezos Blockchain

The security inherent in Blockchain and distributed ledgers fits e-commerce like a glove. I predict it won’t be long before Amazon owner, Jeff Bezos, will try (and probably succeed, given his track record) to create the Amazon Blockchain, the blockchain for secure online commerce.

I also predict someone like Larry Ellison, the guy in charge of the world’s largest financial software company, Oracle, will connect businesses and government/federal tax systems in a fraud-free, software-driven ecosystem via the Oracle Blockchain (and will probably buy another Hawaiian island with the profits…). Imagine that, a system that disallows the sort of tax loopholes that is keeping “more than 2 trillion dollars” of profits away from the US economy.

Come on, though. Is it really the end for banks?

Smart investors never put all their money into one stock, it’s an eggs-in-basket thing. Spreading your risk across multiple holdings just makes good sense.

This summer I know lots of people in the UK who ‘bought some dollars’ to tie their wealth to, as the British Pound slid after the Brexit referendum result.

And it’s probably going to go the same way with cryptocurrencies and blockchain. No, it’s not really the death of banks; I expect people will begin to split their cash between a cryptocurrency and traditional currencies until one or the other becomes the de facto winner.

But then, if blockchains weathers the initial doubts, we might start seeing a shift in financial power away from centralisation and more towards democratised, distributed ledgers, where fraud is impossible, and every digital cent can be accounted for.

Y’know, “Amazon World Bank” has a certain ring to it…